To be completely frank, I was a bit of an idiot in March. Not totally, I’ll get into it in the breakdown, but some of it was just me not thinking. I’m really working on tightening the belt in April, May, and June so that I can have fun on what is working out to be a whirlwind trip in July.

March Review

I have bought a tracker template off Etsy, I got tired of trying to figure out how to get my graphs to look the way that I want them to and just the time that I’m spending trying to get it to work is way more valuable than the $5 I spent on the tracker. Once I try it out I will let you know what I think.

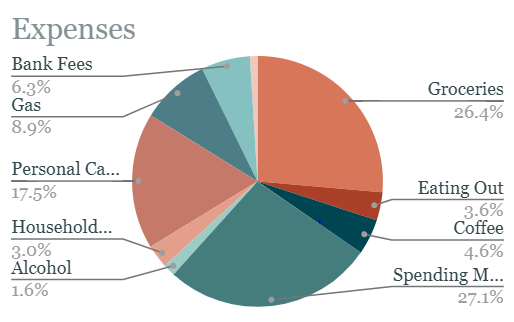

Anyways, that tangent was to explain why my bills are not included in that pie chart, because I am excited about it being April because I can start turning my heat off and slash my electric bill since I won’t need to heat my apartment with my electric, baseboard heaters anymore and I am so glad about that. I’m hoping I can bring my electric budget down to about $100 a month. I’ve had it at $200 a month for January, February, and March and I was over every one of those months. So I am looking forward to warmer weather and $75 monthly electric bills.

My problems arose, as usual with my discretionary spending:

I went $127 over on groceries, this is one area I really want to zone in on in April, however I also reduced my budget down $50, I was basically on par with February, however I am really hoping that no longer needing convenience food since my back is basically completely healed and I am back to full activities again, which includes cooking. So I am hoping that buying ingredients again will bring down my grocery bill.

I went $18 over on eating out, I ended up going to Thunder Bay twice in March for appointments and that meant getting lunch there. I just did them as day trips, not overnights to try and save some money, but really only by saving on a few meals and accommodations. It doesn’t really make a difference in the gas department as you will see in my car section. I also surprised myself by going $37 over on coffee. I normally don’t come close to my $75 budget, but I did get multiple coffees on each of my city days plus my usual one a week; and I just remembered that I went to the coffee shop in town a couple Saturdays to do some personal laptop work out of the house.

This is the real kicker, I went nearly $500 over on Spending Money, I way underbudgeted for my piercings. I estimated $150 and it was double that, plus I bought three books, a really cute pair of earrings that I am obsessed with, and a candle. I did a lot of damage in one day. The other thing that was very damage was all of my skincare used up in like a 3-day span. My sunscreen, face oil, cleansing balm, moisturizer, tinted moisturizer, concealer, all of it, so then I dropped nearly $300 in Sephora only buying things I actually needed. It felt terrible.

As previously mentioned, gas was way over, $129 over to be precise. I tried to gas up in more urban areas as often as possible, it’s always 1-20 cents a litre cheaper , sometimes more, but still a round trip almost 800km drive costs money. Which is why I’ve never done it very often.

I was underbudget in alcohol, Montana (my cat), household supplies, and spent nothing out of car maintenance or gifts.

April Planning

There are three main areas I want to greatly cut spending: groceries, spending money, and personal care. Last month, I did not make a “What I’m Buying in March” and I think that is actually a really important tool for planning my spending.

Groceries: I am planning on making a very specific meal plan each week and really sticking to it. I’m thinking that there will need to be about 3 meals a week, some 4-6 portion meals, some 2 portion meals, and at least one of those meals will be vegetarian. I am also going to eliminate my Friday evening grocery shop for “weekend food”. I think it will be better for my waistline and my wallet. This will require serious planning, list making, and sticking to the list. I always forget something when I’m grocery shopping, and then I have to go back and then I end up getting things I didn’t mean to. I also am planning on nixing most of the chocolate. I have a feeling that if I don’t buy as much chocolate I will save a lot of money.

Spending money: I think this is where my “What I’m Buying in March” post comes in, I make a plan, I budget for the plan and I stick to the plan. That’s it.

Personal care: Doing these budget tracking spreadsheets have been illuminating for how much money I spend on personal care products. I seem to very easily spend $200-300 on skincare, makeup, hair stuff each month. I need to make a plan for how to address this, I don’t currently have one. Although, I should not need to buy anything for a while, so I’m hoping that will save me.

Travel: I am hoping to not need to go to Thunder Bay at all in April. However, I do need to buy some plane tickets for summer travel, some of it will be reimbursed, but maybe not for a bit, so I need to figure out how to balance it.

Subscriptions: I have also cancelled renewal on a couple annual subscriptions, The Pilates Class and SkillShare. I will probably re-subscribe to The Pilates Class, I did enjoy it, but I haven’t been using it much lately and I just can’t afford it at the moment. And SkillShare I did not like and never used. I will never be renewing.

So that’s the check-in, I feel like I blew it a bit in March. Like I lost any progress I had been making, but I’m trying to work on not feeling guilty about it, although I very much do.

Have a great month,

Laura

One response to “Financial Fitness Check-In: March 2023”

[…] Financial Fitness Check-In: March 2023 […]

LikeLike