March and April have been such a change from January and February this year that I almost feel like I have whiplash, I definitely still feel confused about so much. Like why do I feel guiltier about spending money, now that I actually have some than I did when I was constantly maxing out my credit card and in overdraft? Now that I have spent some money, how do I make sure I reel it back in so that I don’t end up back where I was? Does anyone ever know if they are doing the right things with their money? How do you decide what is the right thing for you? It’s definitely been causing a bit of an existential crisis over here.

There was one income-based surprise this month, I knew that at some point my unused sick and vacation days would be paid out, because I had accrued too many to carry all those hours over. I was not expecting essentially another pay cheques amount of pay out, so that was a very nice surprise and also a big contributor as to why I “spent intuitively” this month instead of paying close attention to my budget. I also had a long pet sit that I got paid for, technically I had two long pet sits, but one was for a friend so they get a big discount, but that was expected and accounted for.

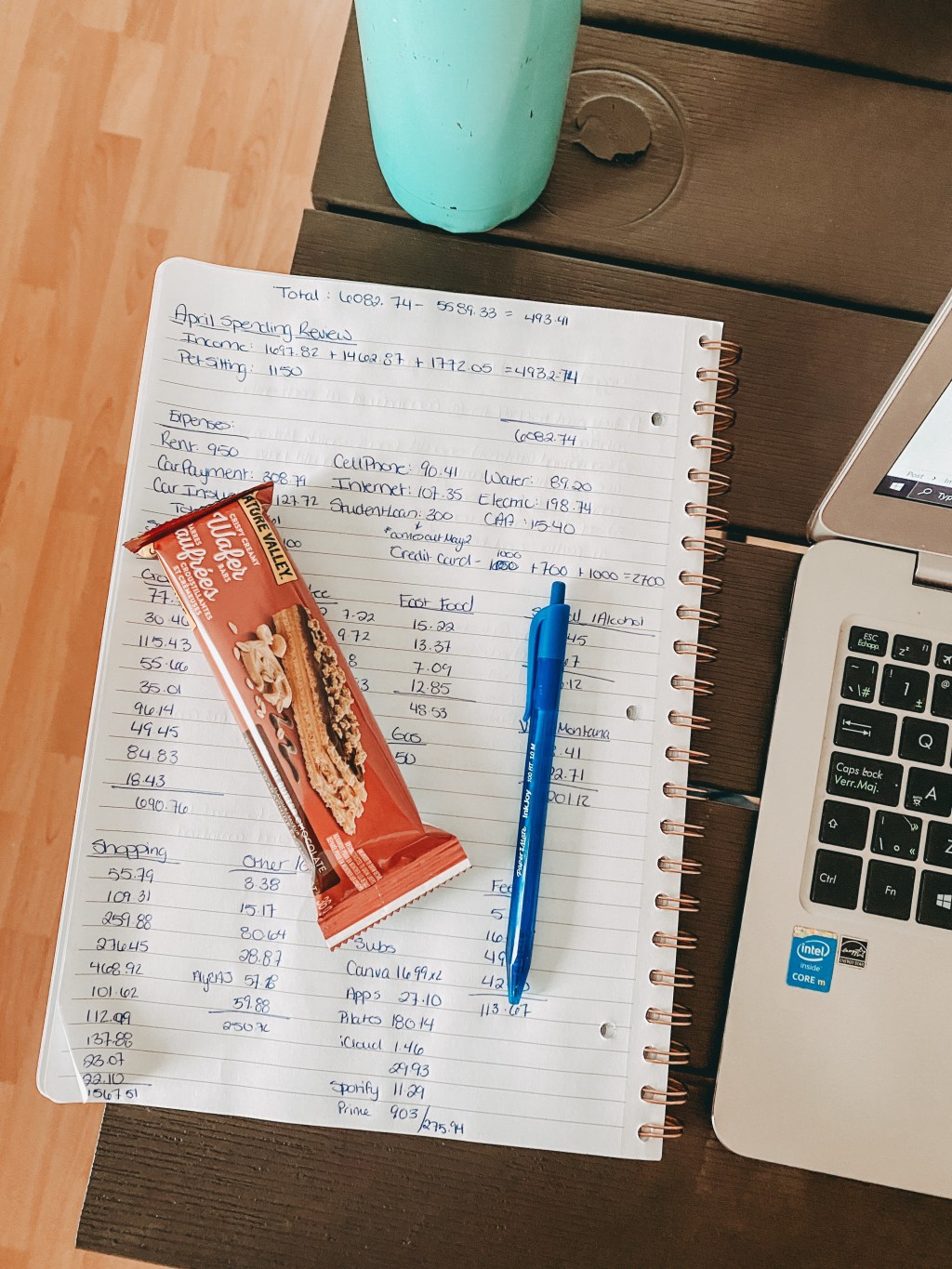

So as you can see, I did some shopping this month. I got some things I’ve been putting off, like a bed skirt to cover up my nasty old box spring, a car phone mount for my new car (the old one didn’t fit into where the air vents are in this one) so that I can actually see maps when I’m driving somewhere new, some new clothes, basics that were greatly needed, shopped the Sephora sale, bought and mailed some presents (regret, people are getting e-gift cards from now on, postage is insane!), paid an annual subscription to The Pilates Class, bought concert tickets for June, and took Montana to the vet.

I think the biggest take away I have from the past couple months, is that if you can get to a point where when you get money you don’t need to spend it, that is true financial freedom. And I don’t know if we as humans generally have that stopping point, because look at the super yachts and gold toilets of the world. But if when you get some money and some flexibility in your budget you don’t have a list of things that are needs, like I need something to hold my phone up so that I can use it for maps while driving without getting a ticket, I need to exercise, I literally needed clothes that fit me properly and I feel comfortable in. Montana needed food and to go to the vet. Maybe I don’t need to go to concerts, or pay for Spotify, wax my upper lip (realistically I could pluck the one black hair), or to get coffee out once a week, but those are also the things that give me hope each week, so in a way they are needs. And things have been so tight for so long that it is really, really nice to not feel guilty about that.

Savings

For my savings goals I am currently working towards a $1000 emergency fund, it currently has $657. 08 in it. So not too shabby.

I started putting money into my travel savings account again for the first time since before my surgery in October 2020, I’ve decided so far at $50/paycheque. It is currently sitting at $101.01. I don’t know for sure what my goal is here.

And then in my other savings account, which doesn’t 100% have a purpose, I guess it would be my moving fund? or my rainy day savings? I’m not certain, sometimes I think I should be putting it on my credit card since it doesn’t really have a purpose, but it is currently sitting at $426.01.

Looking at that I cannot believe that in February both all of those accounts were at $0 and my chequing was consistently in the negatives. I know it’s not a lot, and that one emergency would wipe me out, but it feels really good to have made that progress in 2 months, and have paid off my credit card and bought things I needed.

Credit Card

I have a credit limit of $4000, I am currently sitting at $2900 at the end of the month. Given that I had gotten it down to about $2100 mid-month, I am a little bummed about that, but I’ll be making a payment this Friday, and since I have work travel again, I’ll have a little extra in my next pay cheque. I’m also considering doing a no spend month again, since I have spent so much in the last couple months. I’m not sure. I feel like I need to spend some serious time at home and get settled back into my apartment and my normal life again. But I am just also thrilled that I’m not over the limit like I so often was last year, and my credit score has gone up 30 points in the past two months.

May Goals

This is going to be a much more normal month income-wise, I don’t have any paid pet sitting booked for the month, just one night for a friend that I won’t charge her for. And then I’m considering stopping the pet sitting, although I do have one job booked in June (partly to help me recover from my Minneapolis trip). So I want to make sure that after the past couple months of having much more income than normal I remind myself to live within my means. Although thinking about that I just remembered I do also have my tax return coming and I need to plan what to do with it.

Spending wise, I’m excited that my electric bill will be going down, there’s still snow on the ground, but you can definitely tell that spring is coming which means we can turn the heat off and get away from the $300 electric bills. And then groceries, I say this every month, but I think that May needs to be the month that I really sort out that spending. I don’t know if it’s inflation, living in the North, or me, but I spend way too much on food for a single person and I can really make a change in my savings/debt repayment if I can get that down to a more reasonable number.

There’s always something else to think about, isn’t there?

Laura