As a part of working to pay off my debt and generally “get ahead” I have established a pay week routine to help me plan in detail where every dollar is going.

Essentially it’s part of a zero-based budget routine. Which many finance people talk about, but Dave Ramsey is one of the biggest proponents of. Like many people, I think Dave Ramsey has a point, but I also think that getting out of debt is a lot like a diet. When you crash diet, you often end up binging, but when you slowly and steadily lose weight you can often keep it off long term. Intuitive eating, where you honour your hunger cues, eat what you want, when you want it and practice gentle nutrition has actually been shown to help heal disordered eating patterns. So, if we follow that model for spending and getting out of debt, I think there is a chance that it could maybe create a healthy relationship with spending and debt.

Also, I just can’t believe that my one weekly coffee is what is keeping me in debt. And if a weekly latte helps to motivate me then I will sacrifice the $6. I’m also not about to start tithing (giving 10% of my income to church), which is one of the infamous Baby Steps.

Anyways, circling back to the pay week planning. We get our pay stubs emailed to us on Wednesday, so that is the day that I do my planning. I always make sure to check my vacation hours, sick hours, and accrued compensatory time-off (CTO), this is time that instead of getting overtime paid out I can accrue it and earn more than my contractual time off. I typically ask for my CTO to get paid out. Especially at the moment as our fiscal year ends at the end of March, and there literally are not enough days for me to take off all the hours I would have accrued. I can’t even take off all my normal contractual vacation days in the days we have left in March (although I am taking some time off).

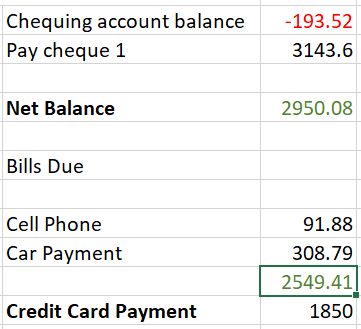

So, once I have checked through my pay stub and made sure that all the deductions are correct and my vacation time is correct I get out a piece of scrap paper. I check the balance in my chequing account (where my pay cheque goes), write that down as my current balance and then write down my net pay amount and add them together, that is the amount that I am working with for the next two weeks. That may seem obvious, but when you are often in the negative bank balances by the end of a pay period, you need to know what you are working with, to try and figure out how to pay all your bills, eat and stay in the positive for the next pay period.

From there I look at what bills are happening in the pay period. Typically, that looks like:

Pay 1: car payment, car insurance, water, electric, cell phone, and internet

Pay 2: rent and student loan

That looks like an uneven division of bills, but in terms of amounts they work out pretty evenly.

Once I have my “working balance”, I subtract all the bills that I pay out of my chequing account. I pay some bills out of my chequing and some via credit card. And I would love to someday be at the point where I pay my credit card off in full every month, but I’m not there yet and so for the moment I don’t subtract those from my working balance, which leads me into:

Calculating my credit card payment. So once I have subtracted my bills from my “working balance” I then, hopefully have a decent amount of money left. From there I figure out how much money I need to live on for the next two weeks, groceries, cleaning and hygiene supplies, pet food, maybe a bit of fun etc. And the rest becomes my credit card payment for that pay cheque. That’s a lot of words to describe what essentially looks like this:

With a big, big asterisk that my pay cheques are not normally 3k each, this is close to double what I normally make in a pay period thanks to working on a stat holiday, nearly 80 hours of overtime, and our bonus COVID pay for when we are on the frontlines of an outbreak response. I am super pleased because it will actually allow me make a big dent in paying off my credit card.

My first pay cheque of the month is typically the one that I can “do stuff” with, I can get stuff for my apartment, get cat food, beauty supplies, make a big credit card payment, you know, do stuff with. The second cheque of the month is typically rent, student loan, and groceries for the two weeks. If it’s a magical three cheque month, then I use that cheque to play with a bit.

So that’s it, that’s the pay stub portion of the routine.

Then on Friday morning when I wake up to money in my bank account I implement the plan. I pay any bills that I have to manually pay, transfer money to my credit card to make a payment. It means that I don’t have to think. I know that some people have automatic transfers set up, but I am not yet at a point where I can have the same amount transfer out every pay cheque (I also can’t figure out how to do it with my bank).

So that’s it for my pay week routine, typing it out and reading it over it seems like a lot. It would be cool to be able to simplify this a lot.

Do you have any tips on simplifying your financial routines?

Laura